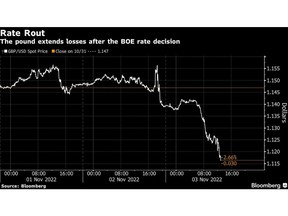

The Bank of England’s jumbo rate hike failed to buttress the pound, which extended the biggest slump this week among major currencies as UK policy makers challenged the market’s view on the scale of future increases needed to tame inflation.

(Bloomberg) — The Bank of England’s jumbo rate hike failed to buttress the pound, which extended the biggest slump this week among major currencies as UK policy makers challenged the market’s view on the scale of future increases needed to tame inflation.

Advertisement 2

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

The Monetary Policy Committee voted 7-2 to lift rates by 75 basis points to 3%, the highest level in 14 years. But in an unusually direct comment on investor predictions for future hikes, it said peak rates will be “lower than priced into financial markets.”

Financial Post Top Stories

Sign up to receive the daily top stories from the Financial Post, a division of Postmedia Network Inc.

By clicking on the sign up button you consent to receive the above newsletter from Postmedia Network Inc. You may unsubscribe any time by clicking on the unsubscribe link at the bottom of our emails. Postmedia Network Inc. | 365 Bloor Street East, Toronto, Ontario, M4W 3L4 | 416-383-2300

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Financial Post Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

“This is as dovish a hike as can be,” said Axel Botte, global strategist at Ostrum Asset Management. It’s “quite unusual for a central bank to comment on market rate expectations so bluntly,” he said.

The pound was already down in Thursday’s session after hawkish comments by US Federal Reserve Chair Jerome Powell on Wednesday lifted the US currency. The pound extended its slide after the BOE’s decision, trading more than 2% weaker at $1.1157, the lowest since Oct. 21. The currency is poised for a 3.7% slump in the week. Yields on short-maturity government debt fell after the decision, while longer-dated yields climbed.

This advertisement has not loaded yet, but your article continues below.

Article content

Here’s what strategists and economists have to say:

Jane Foley, senior FX strategist, Rabobank:

“The upshot is that today’s move has been perceived as a dovish hike by markets and once again GBP is reacting to the gloomy projections from the Bank, rather that to the fact that Bank rate is now higher — albeit to a level that was already priced in.”

Jordan Rochester, currency strategist at Nomura Holdings Inc.:

“We have $1.05 by year-end, based on falling global growth, and the BOE is helping here. The difference to Powell last night is striking: Europe — ‘we’re being forced to hike’ and we don’t like it, versus the US — ‘pls stop telling us we’re pivoting!’

“If you buy GBP here it’s because you think 1) US Core CPI decelerates a lot (the year of upward surprises is over) or growth rebounds, 2) Energy prices will collapse (front end natural gas is rising again), 3) Peace in Ukraine (if anything noise over nukes increasing), 4) UK assets look cheap — I’d be worried about UK credit risks here, insolvencies are on the rise to 2008 levels.”

Advertisement 4

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Antoine Bouvet, senior rates strategist at ING Bank NV:

“It seems like each time there is a gilt selloff, the back-end lags. It still feels like this is the weak spot on the curve. This is despite the BoE not selling gilts in the sector as part of QT. At least it vindicates their decision to focus on shorter tenors.”

Jamie Dutta, market analyst, Vantage:

“The difference in rhetoric between yesterday’s Fed meeting pushing the peak rate higher and today’s decisions from the BOE pushing market pricing lower is stark. GBP/USD has rolled over and fallen over three big figures since Fed Chair Powell began his press conference. Bears will target 1.10 in the near term.”

Valentin Marinov, head of G10 currency research at Credit Agricole:

This advertisement has not loaded yet, but your article continues below.

Article content

The BOE is “sending a clear signal that the Bank Rate path expected by the markets ahead of the policy meeting is too high. The outcome contrasts sharply with the hawkish message from Fed Chair Powell yesterday and could trigger further drop of the GBP-USD rate spread, adding to the headwinds for GBP/USD.”

Hugh Gimber, global market strategist at J.P. Morgan Asset Management:

“A more modest hike today, when inflation is pushing further into double digits and following strong action from both the Federal Reserve and the European Central Bank, would have risked reigniting questions about the Bank’s credibility and further volatility in sterling markets. All eyes will now turn to the fiscal statement on 17 November, where the Chancellor will need to strike a fine balance between supporting the economy and a credible medium-term plan for debt consolidation.”

Advertisement 6

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Axel Botte, global strategist at Ostrum Asset Management:

“This is as dovish a hike as can be. BoE seems to discard the inflationary impact of current fiscal stance (however revised, still much easier than in August when they issued the last inflation report). Quite unusual for a Central Bank to comment on market rate expectations so bluntly. Too dovish, QT will exert some pressure on intermediate bonds. Inflation expectations will move up further.”

Dan Boardman-Weston, CEO and chief investment officer at BRI Wealth Management:

“The Bank has a difficult balancing act though as the current cost of living crisis combined with higher interest rates and higher taxes means that the growth outlook for the UK is gloomier than it has been since the dark days of Covid, and we’re likely to see a continued slowdown in economic activity over the coming months.

Advertisement 7

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

“Inflation continues to be largely supply driven and interest rate increases are not going to assist with these contributory factors to inflation. Whilst we have more political stability than we have done for some months, economic instability unfortunately continues.”

Marc Ostwald, chief economist and global strategist at ADM Investor Services Int:

“I would say the forecasts are even more dire than most had expected, but thus far market peak assumption only dialed back slightly 4.6% peak vs. 4.7% pre-meeting. I think it also reflects the fact that everything is still really hanging on what happens in fiscal terms. It’s all very well for Sunak and Hunt to talk about sorting out the financing gap, but will the backbenchers vote for that level of austerity with an election just 2 years away.”

Advertisement 8

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Jeremy Batstone-Carr, European Strategist at Raymond James:

“There is no doubt we are now looking down the barrel of a recession, which is unfortunately a necessary by-product of the policies required to restore fiscal credibility. The aim is stability in the long-term, as further highlighted by the Bank beginning quantitative tightening, with the Bank hoping the economy will rise out of the recession by this time next year.”

Tim Graf, head of EMEA macro strategy, State Street:

“We doubt we will see further hikes of this magnitude. Data capturing consumer activity are already showing signs of significant weakness and the all-important housing sector will surely become more vulnerable the further and faster rates rise. Terminal rate pricing closer to 4.00-4.25% (from 4.75% prior to the meeting) now seems the more likely end state for policy rates, implying more modest tightening ahead.”

(Adds strategist comments)

Share this article in your social network

Advertisement

Story continues below

This advertisement has not loaded yet, but your article continues below.