All eyes will be on the Bank of Japan when it sets policy on Tuesday, as Governor Kazuo Ueda continues to inch toward ending the world’s last negative interest-rate regime.

(Bloomberg) — All eyes will be on the Bank of Japan when it sets policy on Tuesday, as Governor Kazuo Ueda continues to inch toward ending the world’s last negative interest-rate regime.

Chances are it won’t happen this time. People familiar with the matter indicate that Japanese authorities aren’t in a hurry to move while they await hard evidence of sustainable inflation.

Advertisement 2

Story continues below

This advertisement has not loaded yet, but your article continues below.

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Exclusive articles from Barbara Shecter, Joe O’Connor, Gabriel Friedman, Victoria Wells and others.

Daily content from Financial Times, the world’s leading global business publication.

Unlimited online access to read articles from Financial Post, National Post and 15 news sites across Canada with one account.

National Post ePaper, an electronic replica of the print edition to view on any device, share and comment on.

Daily puzzles, including the New York Times Crossword.

REGISTER TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account.

Share your thoughts and join the conversation in the comments.

Enjoy additional articles per month.

Get email updates from your favourite authors.

Article content

Article content

BOJ watchers will therefore scour the statement and comments by Ueda for hints on the outlook for wage hikes and the prospects for better pay spurring spending and demand-led inflation.

Any bullish rumblings will underpin growing expectations that the BOJ will raise its rate no later than April, as predicted by two-thirds of economists surveyed by Bloomberg earlier this month.

“We have argued that Ueda would move gingerly toward exiting the stimulus program he inherited, using a policy review and deliberate signaling to prepare the market well in advance. This process has clearly begun – but is a long way from over.”

—Taro Kimura, senior Japan economist. For full analysis, click here

On the surface, the BOJ’s mission may seem a little awkward after the US Federal Reserve telegraphed rate cuts in 2024.

It’s important to remember that the BOJ has no intention of introducing restrictive settings. If and when Ueda ends the negative rate, the governor will emphasize that policy remains broadly stimulative.

Elsewhere, the latest evidence of price pressures from the US to the UK, a rate hike in Turkey, and cuts in borrowing costs from Hungary to Chile may keep investors focused in the last full working week of the year for much of the world.

Top Stories

Get the latest headlines, breaking news and columns.

By signing up you consent to receive the above newsletter from Postmedia Network Inc.

Thanks for signing up!

A welcome email is on its way. If you don’t see it, please check your junk folder.

The next issue of Top Stories will soon be in your inbox.

We encountered an issue signing you up. Please try again

Article content

Advertisement 3

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Click here for what happened last week and below is our wrap of what’s coming up in the global economy.

US and Canada

The US will get its last major inflation reading of the year with the personal consumption expenditures report, the Fed’s preferred gauge.

The PCE price index is seen stalling for a second month in November, while the core measure that strips out food and energy prices will probably rise 0.2%.

Both metrics are expected to ease on an annual basis, further supporting expectations for a soft landing in the wake of the Fed’s pivot toward rate cuts.

There’s also a flurry of real estate data on tap, with homebuilder sentiment, housing starts and both new- and existing-home sales all coming. Atlanta Fed President Raphael Bostic is scheduled to speak on Tuesday.

Turning north, Statistics Canada is set to release a raft of economic data before closing up shop for the holidays. It will reveal whether inflation continued to slow in November after decelerating to a 3.1% annualized pace the previous month.

Separate reports on retail trade and gross domestic product for October will offer further insight into Canada’s softening economy.

Advertisement 4

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

The Bank of Canada is also set to release a summary of the deliberations that led to its Dec. 6 decision to hold its key rate at 5%.

For more, read Bloomberg Economics’ full Week Ahead for the US

Asia

The BOJ gets an update on national inflation trends on Friday, with the pace of gains for prices excluding fresh food seen moderating to 2.6% in November.

Elsewhere in the region, Malaysia’s consumer-price index for November is due the same day.

The rest of the week’s slate is heavy on trade. Having dropped for 13 straight months, Singapore’s non-oil exports for November are due on Monday.

New Zealand’s trade balance comes Tuesday, with Japan’s trade account and Taiwan’s export orders for November a day later. Taiwan reports on unemployment on Friday.

The Reserve Bank of Australia releases minutes from its December meeting on Tuesday, and South Korea’s central bank publishes an account of its November meeting the same day. The BOJ releases minutes of its October meeting on Friday.

Bank Indonesia is expected to hold its seven-day reverse repo rate unchanged at 6% on Thursday.

Advertisement 5

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

For more, read Bloomberg Economics’ full Week Ahead for Asia

Europe, Middle East, Africa

With the Bank of England having just pushed back against market bets anticipating rate cuts, data on Wednesday will showcase the challenge faced by officials targeting annual consumer-price growth of 2%.

While inflation is expected to have slowed in November, economists still anticipate that it remained above 4% — while the core measure is seen staying above 5%.

In the euro zone, Germany’s Ifo index on Monday will indicate whether business sentiment is improving at a time when the economy is trudging through a possible recession.

In the wake of last week’s European Central Bank decision, where President Christine Lagarde also sought to temper wagers on an imminent rate cut, a few other officials are scheduled to make appearances in the run-up to Christmas.

Among them is chief economist Philip Lane, who’ll speak in Dublin on Wednesday and Thursday after chairing a panel at a conference on fiscal policy hosted by the ECB earlier in the week.

In Eastern Europe, Hungary’s central bank may deliver its final rate cut of the year on Tuesday, as drastically slowing inflation and the arrival of European Union funds widen room for monetary easing.

This advertisement has not loaded yet, but your article continues below.

Article content

On Thursday, the Czech central bank decision is expected to be a close call on whether it too should start cutting borrowing costs.

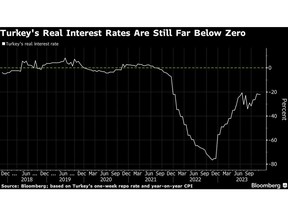

In Turkey the same day, monetary officials may continue extreme tightening. They’ve already raised the key rate by almost 32 percentage points since June to counter soaring inflation and encourage foreign investors to return. The consensus is for a move of roughly 250 basis points.

Also on Thursday, Egyptian monetary authorities make their first decision on borrowing costs since a presidential election that President Abdel-Fattah El-Sisi is all but assured of having won.

Facing an economic crisis and inflation of about 35%, authorities are expected to devalue the pound in the coming months and may also look to raise the key rate, which stands at 19.25%.

For more, read Bloomberg Economics’ full Week Ahead for EMEA

Latin America

Early Tuesday, Brazil’s central bank posts the minutes from its Dec. 13 decision to deliver a fourth straight half-point cut, which trimmed the key rate to 11.75%.

Economists surveyed by the central bank see 250 basis points of easing in 2024 but much less space for cuts in 2025 and 2026.

Advertisement 7

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Brazil’s central bank also publishes its quarterly inflation report, which will serve up technical assessments, scenario analyses and updated economic forecasts.

On the inflation front, Mexico posts mid-month inflation prints that are once again expected to trend lower after a modest re-acceleration in November. Mexico, along with Argentina and Colombia, will also report October economic activity data.

Sticky inflation readings in Colombia have economists divided over whether Banco de la República begins to unwind a record tightening cycle on Tuesday. Minutes of the gathering will be published late Friday.

In Chile, an unexpectedly modest slowing in inflation last month prompted economists surveyed by the central bank to scale back their rate cut forecast for Tuesday’s meeting to 8.5% from last month’s 8.25% estimate.

For more, read Bloomberg Economics’ full Week Ahead for Latin America

—With assistance from Robert Jameson, Laura Dhillon Kane, Molly Smith, Piotr Skolimowski, Vince Golle and Paul Wallace.

Comments