Article content

(Bloomberg) — OPEC+ is still finding that the best response to growing oil market uncertainty is to hold its ground.

(Bloomberg) — OPEC+ is still finding that the best response to growing oil market uncertainty is to hold its ground.

Story continues below

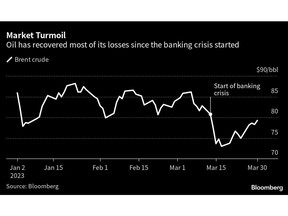

When last month’s banking crisis dragged crude futures to a 15-month low near $70 a barrel in London, speculation swirled that Saudi Arabia and its partners might intervene with fresh production cuts to shore up the market.

But despite all the upheaval, OPEC+ shows every sign of sitting tight. The Saudis have said publicly that the 23-nation coalition should keep output levels steady all year. Delegates privately predict that, when key members hold a monitoring meeting on Monday, they won’t make any adjustments.

Fears over financial contagion are receding and the focus is returning once again to China’s resurgent oil demand, coupled with pressure on Russian output since its invasion of Ukraine. Crude futures have recovered sharply to almost $80 a barrel, buttressing revenue for Riyadh and its allies.

Story continues below

“OPEC can intervene with markets when it feels there’s an oversupply,” said Marco Dunand, chief executive officer of commodities trader Mercuria Energy Group Ltd. But “it’s more likely that once we go through this, we’re going to see the market coming back up.”

The oil-market outlook confronting the Organization of Petroleum Exporting Countries and its partners remains cloudy.

Confidence that prices were heading back to $100 a barrel, widespread in the petroleum industry at the start of the year, has frayed as Russian exports prove resilient against international sanctions. It looks like global supply will be in surplus this quarter.

China’s modest new economic growth target of 5% has also sapped optimism among oil investors. Even Goldman Sachs Group Inc., perhaps the most enthusiastic crude bull on Wall Street, has dropped predictions of a return to triple digits this year.

Story continues below

The reverberations from the collapse of Silicon Valley Bank and unraveling of Credit Suisse Group AG further darkened crude’s prospects.

Test of Resolve

There was speculation that the price rout could test the resolve of Saudi Energy Minister Prince Abdulaziz bin Salman, who said last month that the production targets fixed when OPEC+ slashed output in late 2022 are “here to stay for the rest of the year, period.”

Those predictions have diminished amid crude’s subsequent recovery.

“The OPEC leadership will very likely decide that there is no need to exercise the additional cut option” next week, said Helima Croft, head of commodity strategy at RBC Capital Markets LLC. “But we do not see the group remaining on autopilot until year-end if oil descends into another tailspin.”

Story continues below

Top oil traders like Trafigura Group Pte Ltd. and Gunvor Group don’t expect a further price slump. In fact, they predict a rally in the second half of 2023 as China fully emerges from years of Covid lockdowns. Goldman Sachs, while softening its initial price expectations, has doubled down on calls for a commodities boom.

Global oil demand remains on track to increase by 2 million barrels a day this year to a record 102 million a day, shifting the market into a deficit this summer, according to the International Energy Agency in Paris.

The robust outlook for oil consumption comes alongside a pinch on global supplies.

Russia, a member of the OPEC+ alliance, has announced a production cutback of 500,000 barrels a day this month in retaliation for sanctions, and promised to keep the reduction in place through to June. European nations have banned Russian barrels, and only provide facilitating services to countries that purchase shipments for less than $60 a barrel.

Story continues below

While the country’s oil industry has so far defied predictions of a collapse by diverting crude flows Asia, there are signs that the trade is slowing down, with fuel cargoes floating idle off the coast of Europe, Africa and Latin America.

Further disruption is being felt in OPEC member Iraq. A renewed legal dispute between Baghdad and the country’s northern Kurdish region is locking in about 400,000 barrels a day that would normally flow through via Turkey to international markets.

When OPEC+ meets in early June to review output levels for the second half, it may have an opportunity to open the taps. In the meantime, ministers are likely to maintain a wait-and-see approach, according to Bob McNally, president of Rapidan Energy Group and a former White House official.

“I suspect they’ll be keeping their heads down and eyes open,” McNally said.

—With assistance from Salma El Wardany, Ben Bartenstein and Fiona MacDonald.

Comments

Postmedia is committed to maintaining a lively but civil forum for discussion and encourage all readers to share their views on our articles. Comments may take up to an hour for moderation before appearing on the site. We ask you to keep your comments relevant and respectful. We have enabled email notifications—you will now receive an email if you receive a reply to your comment, there is an update to a comment thread you follow or if a user you follow comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

Join the Conversation